- By Ajeet Kumar

- Mon, 01 Jun 2026 03:20 PM (IST)

- Source:JND

- Gen Z globally spends more than they earn.

- Economic pressure, digital influence drive overspending.

- Diversify income, budget, save to build wealth.

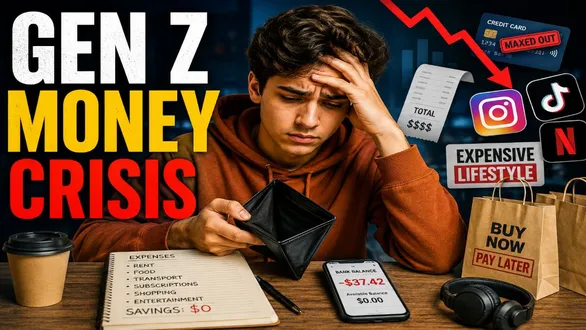

Across the world, Gen Z consumers are spending more than they earn. According to multiple research reports, the young generation is facing a money crisis driven by a combination of economic pressure, lifestyle choices and digital influence. A recent global report by consulting firm Deloitte found that nearly 48 per cent of Gen Zs live paycheck to paycheck, highlighting growing financial stress among young adults. Meanwhile, a 2024 TransUnion survey showed many Gen Z consumers increasingly rely on credit products and buy-now-pay-later (BNPL) services to manage daily expenses.

Why are Gen Z facing money crisis?

Rising rents, inflation and slower wage growth in several economies have made saving difficult. At the same time, social media platforms fuel “comparison culture,” encouraging spending on fashion, travel, gadgets and experiences to match online lifestyles.

ALSO READ: Work, Quit, Travel, Repeat: Why Gen Z Loves Mini-Retirements

A report by the Bank of America Institute also found Gen Z spending growth outpacing income growth in several markets, especially on discretionary purchases. Unlike older generations focused heavily on long-term savings, Gen Z often prioritises experiences, convenience and mental well-being. Experts warn, however, that prolonged overspending and debt dependence could create financial risks if earnings fail to keep pace.

How to save yourself from money crisis

1. Diversification is Key

Don’t depend on one income source or investment. Spread money across savings, investments and side incomes to reduce financial risk. It also includes creating multiple income streams such as freelancing, side hustles or investments. A diversified financial plan helps reduce risk and protects you from sudden job loss, inflation or market downturns.

2. Balance Your Offense With A Strong Defence

Focus on growing wealth through investments, but also build an emergency fund and insurance for financial security. Experts recommend keeping at least 3–6 months’ worth of expenses saved for emergencies. This balance helps you stay financially stable during unexpected events like layoffs, medical issues or economic uncertainty.

ALSO READ: Why Gen Z Is Getting Fired Immediately Globally After Being Hired

3. Optimise Limited Resources

Track spending, cut unnecessary expenses and budget smartly to make the most of limited income and save consistently. Budgeting methods like the 50-30-20 rule (needs, wants, savings) can help maximize limited income and ensure regular savings.

4. Discipline Pays Off

Small, regular savings and controlled spending habits can create long-term financial stability through consistency and compounding. Avoid emotional spending, stick to a monthly budget and automate savings wherever possible. Financial discipline builds long-term stability and helps achieve bigger goals like buying a home, traveling or early retirement.

ALSO READ: Why 'Luxury' Now Feels Like A 'Necessity' For Gen Z And Millennials